When it comes to financial health, most people think only about their personal credit score. But if you’re a business owner or planning to start one, your business credit score matters just as much. Both scores influence how easily you can access loans, credit, or partnerships. Let’s break down the differences and why both are important.

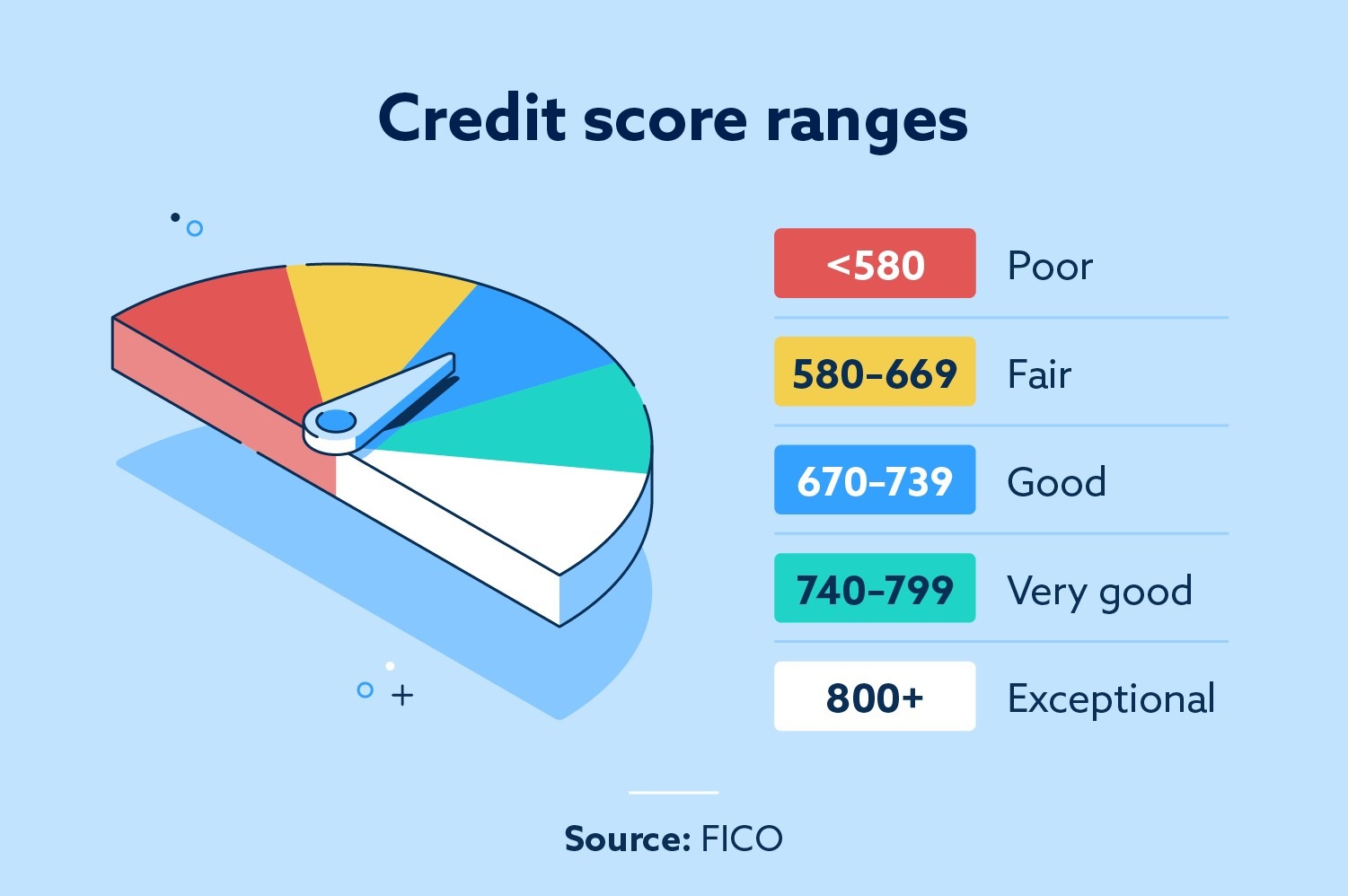

A personal credit score is a three-digit number (usually ranging between 300–900 in India) that shows how responsible you are with money. It is based on factors like:

Timely repayment of credit cards and personal loans

How much of your available credit you use (credit utilization ratio)

Length of your credit history

The mix of credit types (secured, unsecured, revolving)

Number of loan or credit applications made

Lenders use this score to decide whether you qualify for personal loans, credit cards, or mortgages, and at what interest rate.

A business credit score represents the financial credibility of your business. It reflects how reliable your company is when it comes to repaying debts and managing credit. Key factors include:

Repayment track record on business loans and credit facilities

Trade credit history with suppliers and vendors

Company registration details, PAN, and compliance records

Usage of business bank accounts and credit lines

This score plays a crucial role when applying for business loans, vendor credit, government tenders, or partnerships. A higher score makes your business more trustworthy in the eyes of lenders and collaborators.

Many entrepreneurs wonder whether personal and business credit scores affect each other. The answer: yes, in certain cases.

Personal → Business: If you are a sole proprietor or give a personal guarantee for a business loan, lenders will check your personal score. A weak personal score could mean higher interest rates or even rejection.

Business → Personal: If your business defaults on a loan and you’ve personally guaranteed it, the default may reflect on your personal credit as well.

For incorporated businesses, there is usually a separation between personal and business credit. However, lenders often still require a personal guarantee, especially for small or new businesses.

Whether you are salaried or self-employed, your personal credit score impacts your ability to borrow. But if you run a business, having a good business credit score can open more opportunities—like bigger credit lines, smoother vendor relationships, and even better reputation in the market.

Ignoring one can hurt the other. For instance, using your personal account for business transactions may blur the lines and affect both scores. Keeping them separate is a wise step.

For Personal Credit:

Pay your EMIs and credit card bills on time

Keep credit utilization below 30%

Avoid too many loan applications in a short period

Maintain a healthy mix of secured and unsecured loans

For Business Credit:

Register your business formally and use a business PAN

Maintain a dedicated business bank account

Pay vendors and suppliers on time

Keep financial records updated and compliant

In today’s financial ecosystem, both personal and business credit scores are powerful indicators of trust. A strong personal score helps you secure individual credit, while a solid business score builds your company’s credibility. For entrepreneurs, keeping an eye on both ensures smooth access to funding and long-term financial growth.